Authored by Maureen Moran Evans, SVP, Consumer Health, Beauty, and Wellness

Nearly half of 50+ aged consumers say they make the final purchase decision in health, beauty, and food for their household, but 93% say the brand message misses its mark.

Brands often overlook one of the most powerful growth segments in health and wellness: adults over 50 years of age – despite the fact that nearly half of consumers in a new study say they personally make the final purchase decision in health and wellness, food and beverage, and beauty and personal care for their household. The issue is not whether brands can reach the 50+ consumer. It is whether their message truly resonates.

At 55, still working full time and partnering with clients across Food and Beverage, Health and Wellness, and Beauty and Personal Care, I see how brands often strive for broad relevance. But in trying to appeal to everyone, they can unintentionally miss the distinct motivations and expectations of today’s 50 plus consumer.

I have the income. I have the time. I am not slowing down my spending. I am becoming more intentional about where it goes. The data confirms I’m not alone: adults 50 and older report increasing their spending most in food and beverage (32%), health and wellness (30%), and beauty and personal care (29%) over the past year.

People age 55 and older account for more than half of total health spending in the U.S. (56%) while representing just 31% of the population (Kiplinger). We also contribute more than 8 trillion dollars annually to the overall economy. We are not a niche generation. We’re the economic backbone of everyday consumer categories. And we want more.

At Curion, we see this opportunity clearly in the data. In a recent study of more than 7,000 consumers, individuals aged 50 and older reported increasing their spend across food and beverage, health and wellness, and beauty and personal care. The majority of those increasing spend were women ages 54 to 64 with annual household incomes above $75,000 dollars.

Even more important, these same individuals identify themselves as the final purchase decision maker in the very categories where they are increasing their investment.

This is a financially empowered, digitally fluent, highly influential segment driving category growth. And yet there is a disconnect.

These consumers tell us brands focus too heavily on younger audiences. In fact, among adults 50+, the most common sentiment is that brands prioritize younger consumers, while only a small fraction say brands ‘get it right’ and make them feel well represented.

Digging deeper into the same data, we see that fewer than one in ten adults over 50 say brands market to people like them in a way that feels authentic, with 46% of consumers saying “sometimes” or “almost never.”

In other words, there is solid proof that brand and product messaging to this age group often feels inauthentic and the consumers do not feel fully understood. The 50-plus consumer is not aging out of relevance. Brands are aging out of alignment.

I hear this in research, and I feel it personally. When the people increasing spend also feel overlooked, it becomes a growth issue for brands.

Generational Myths That Are Costing Brands

Let’s address the myths still shaping strategy through my 55-year-old lens.

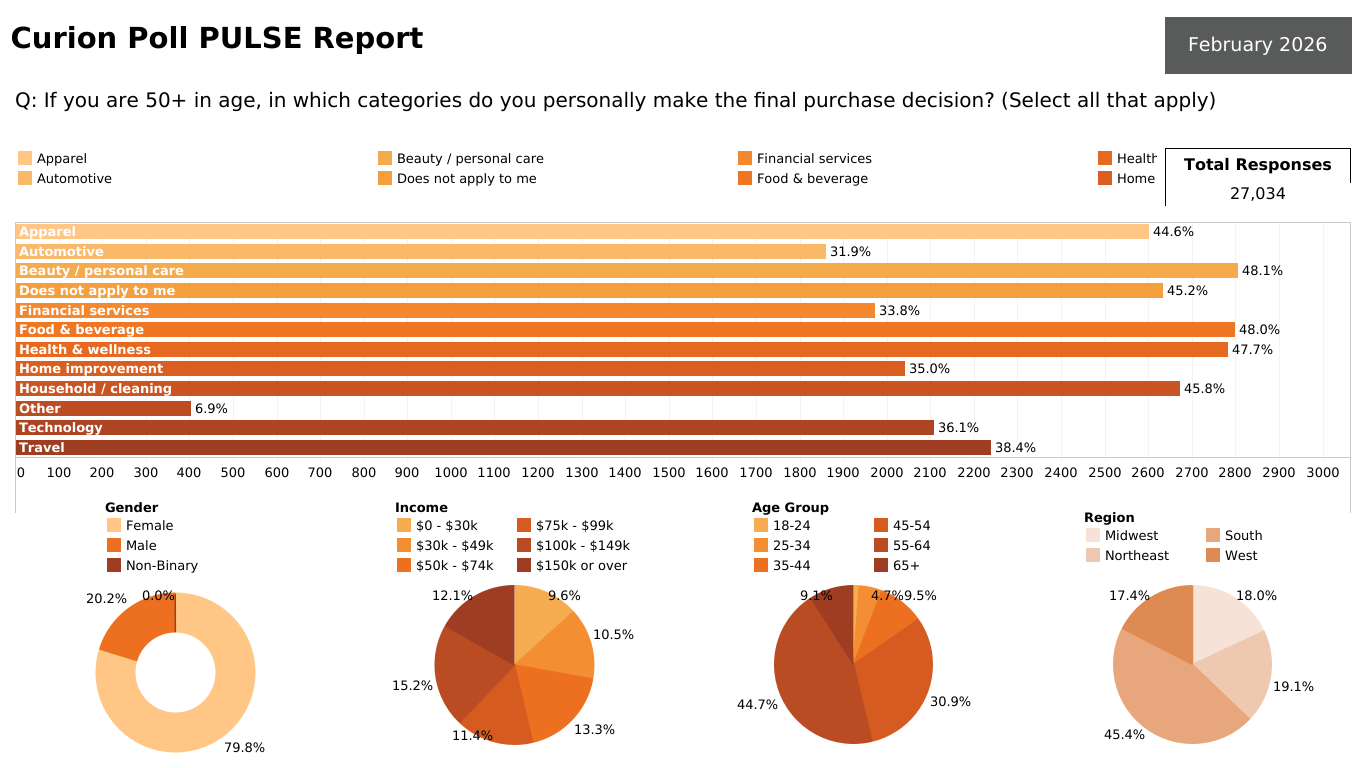

- They do not use technology. Yes, we absolutely do! Adults over 50 are active on smartphones, social media, e-commerce platforms, and telehealth tools. Many of us rely on reviews, tutorials, and digital communities before making purchase decisions. And yet, technology ranks among the categories where more than one‑third (36.1%) of adults over 50 say they personally make the final purchase decision. This comes at a time when online channels already account for a significant share of U.S. ‘everyday staples’ spending.

- They no longer prioritize spending on themselves. The research shows that we are willing to pay more in the very categories leading brands are trying to grow. To be more specific, adults over 50 are increasing their discretionary spend mainly in food and beverage, health and wellness, and beauty categories.

- They are hard to reach. Our media habits are often more stable and less fragmented than younger consumers. In truth, the issue is not “can we reach this demographic?” but rather if the message brands are sending resonates with us. Only a small 6.5% of consumers say brand messaging feels authentically designed for people like them very often. That leaves a whopping 93.5% who feel that brands are missing their mark!

- It is a shrinking segment. Far from it. Demographics tell quite a different story. Longer lifespans and lower birth rates mean this audience is not going anywhere. By 2050, the number of adults over 65 globally will roughly double to about 1.6 billion, reshaping economies and the future of work including in the U.S (McKinsey Health Institute & FII Institute, healthy longevity analysis (2025).

The bottom line is that the narrative many brands still operate from is outdated. The data is not.

Health and Wellness Is the Clearest Opportunity

In health and beauty, the gap between perception and reality is especially visible.

Consumers over 55 are not looking to be told they are aging – we already know that. What we want are products that support vitality, functionality, confidence, and longevity. Many of us are still leading teams, building careers, traveling, investing, and caring for family members. We are not slowing down, but we are recalibrating our priorities.

Yet product positioning often remains narrowly focused on anti-aging tropes or skewed toward much younger life stages.

Representation matters. Authenticity matters. Relevance matters. My generation has significant buying power and long memories. When brands get it right, loyalty follows. When they miss, it is noticed.

Research Is the Unlock

If brands want to close the gap, inclusion cannot be symbolic. It must be intentional.

Adults over 50 need to be prioritized in recruitment and observed in real-life contexts because they are final decision makers across multiple household categories.

- Household/cleaning final decision-maker: 45.8%

- Apparel final decision-maker: 44.6%

- Home improvement final decision-maker: 35.0%

This also aligns with broader U.S. data from Morgan Stanley, showing that these everyday staple categories are where adults over 50 concentrate a large share of their recurring spend as well as act as the final decision maker.

How we shop. How we use products. How we integrate wellness into daily routines while balancing work and life. These insights change packaging decisions, messaging strategies, and innovation roadmaps.

The Real Competitive Advantage

Engaging the 50 plus consumer doesn’t mean brands need to shift away from younger audiences. But rather, expanding the lens.

When brands design for usability, credibility, and authenticity, everyone benefits.

The silver generation is not past prime. It is in peak prime. Financially strong. Curious. Engaged. Motivated to invest in well-being. In fact, global longevity research positions older consumers as one of the most powerful growth opportunities of the next quarter‑century, with healthy longevity framed as a high‑return investment rather than a cost center (McKinsey).

The research confirms it. The market trends support it. And as a 55-year-old consumer, I live the opportunity and the challenge every day. We are not slowing down, and neither is our spending power. Brands that truly want growth must speak to who we are today, not outdated assumptions of the past.

The question for brands is simple. Will you continue marketing around a consumer who controls the final decision in nearly half of everyday purchases – or start growing with them?